We’re now nine years into the current beef price cycle. As we move toward the end of this price cycle and into the next price cycle, cattle producers need to take a good, hard look at where we are — and where we may be going over the next few years.

Throughout most of my professional career, I have encouraged ranchers to develop a management strategy that makes the cattle cycle work for them rather than against them. It is now time to develop that next plan again.

Economic value of a heifer calf

An economic study I completed a couple of years ago focused on the long-run economic value of bred heifers brought into the herd, producing seven consecutive calves. I argue that the lifetime economic value of a bred heifer is the sum of the net incomes she generates while in your herd.

Certainly, a heifer that produces her calves through the top of the price cycle has a higher lifetime economic value than a heifer that produces her calves through the bottom of the price cycle. My study suggested that the most valuable heifer calf born in a herd was a heifer calf born in 2010. These heifers hit their peak economic production during the high prices of 2012, 2013 and 2014.

Contrast this with a 2013-born heifer that was developed in 2014 and started calving in 2015, 2016 etc. My observations were that market prices for bred heifers were just the opposite. Food for thought — nationally, we expanded the herd after the peak prices of 2014.

I plan to update this study in the near future and hope to write a Market Adviser column expanding on the details. For now, let me just say that during a price cycle, the time when a female calves has a major impact on the economic value of that female to a rancher.

Thus, I argue that ranchers need to have a general feel for where we are in the current beef price cycle — and even more importantly, where we might be going in the beef price cycle over the next several years.

Holding back heifer calves at the bottom of the beef price cycle that will calve during the higher calf prices of the next beef price cycle makes a lot of economic sense. Holding back heifer calves at the top of the beef price cycle, like 2014, does not make near as much economic sense.

Biology of cattle cycles

Let’s take a look at the biological factors that cause cattle numbers to change.

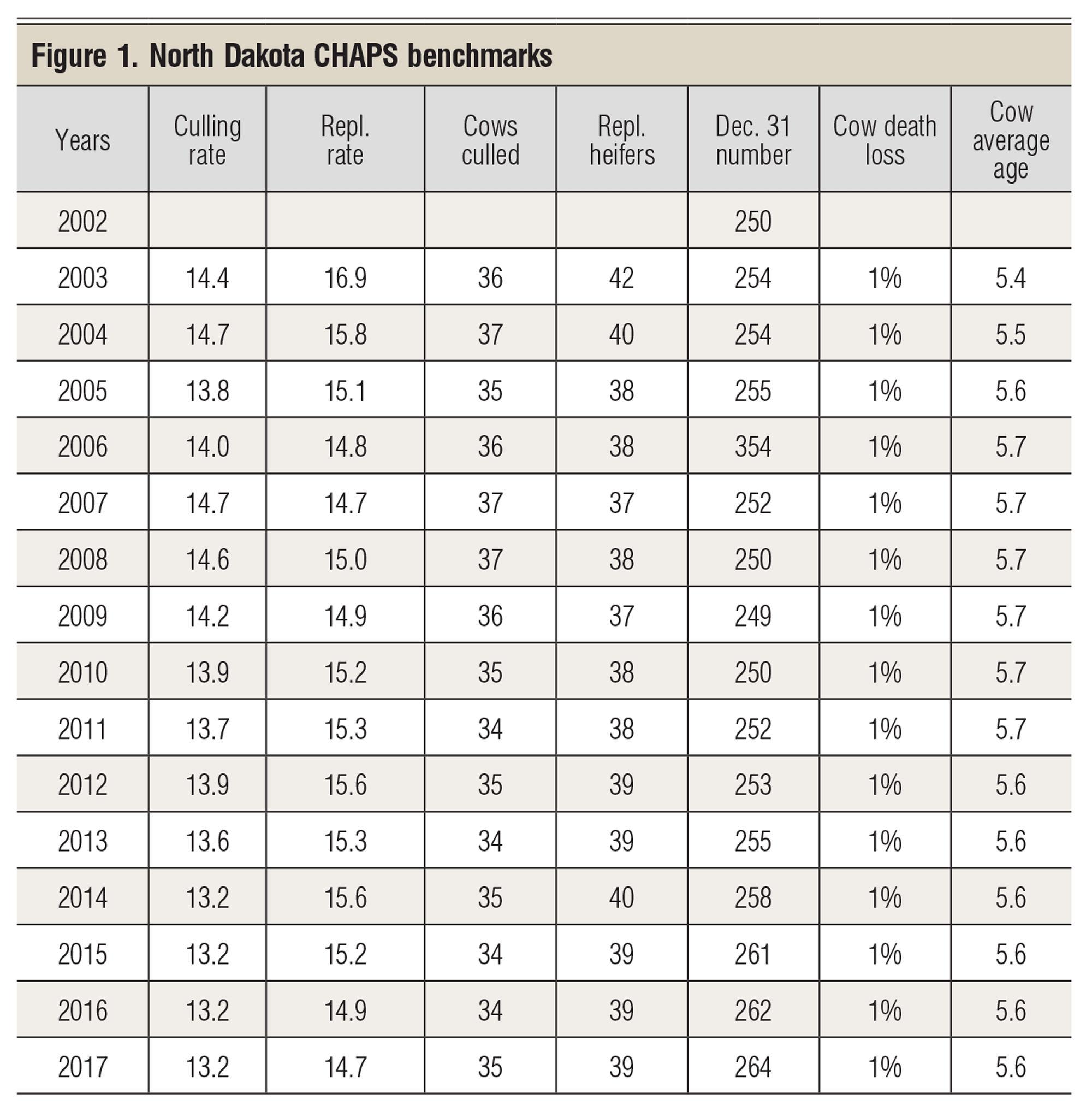

North Dakota Cow Herd Appraisal Performance Software (CHAPS) benchmarks give us some clues of why cattle numbers change over time. Let’s look at the collective culling rate and collective replacement rate for North Dakota’s CHAPS herds.

As cattle producers respond to economic as well as weather forces, they collectively generate a group culling rate and a group replacement rate. These two collective rates tend to be different. Depending on the relative value of these two collective benchmark numbers, the beef cow herd either grows or decreases.

Figure 1 presents CHAPS benchmark data for North Dakota’s participating herds for 2003 through 2017. Columns 2 and 3 present CHAPS collective benchmark averages for the herds’ collective culling rate and replacement rates.

When the replacement rate is higher than the culling rate, beef cow numbers increase. When the replacement rate is below the culling rate, beef cow numbers decrease. I argue that economic prices and the weather are the two driving forces affecting culling rate and replacement rate. Prices tend to move nationwide, while weather tends to change by regions.

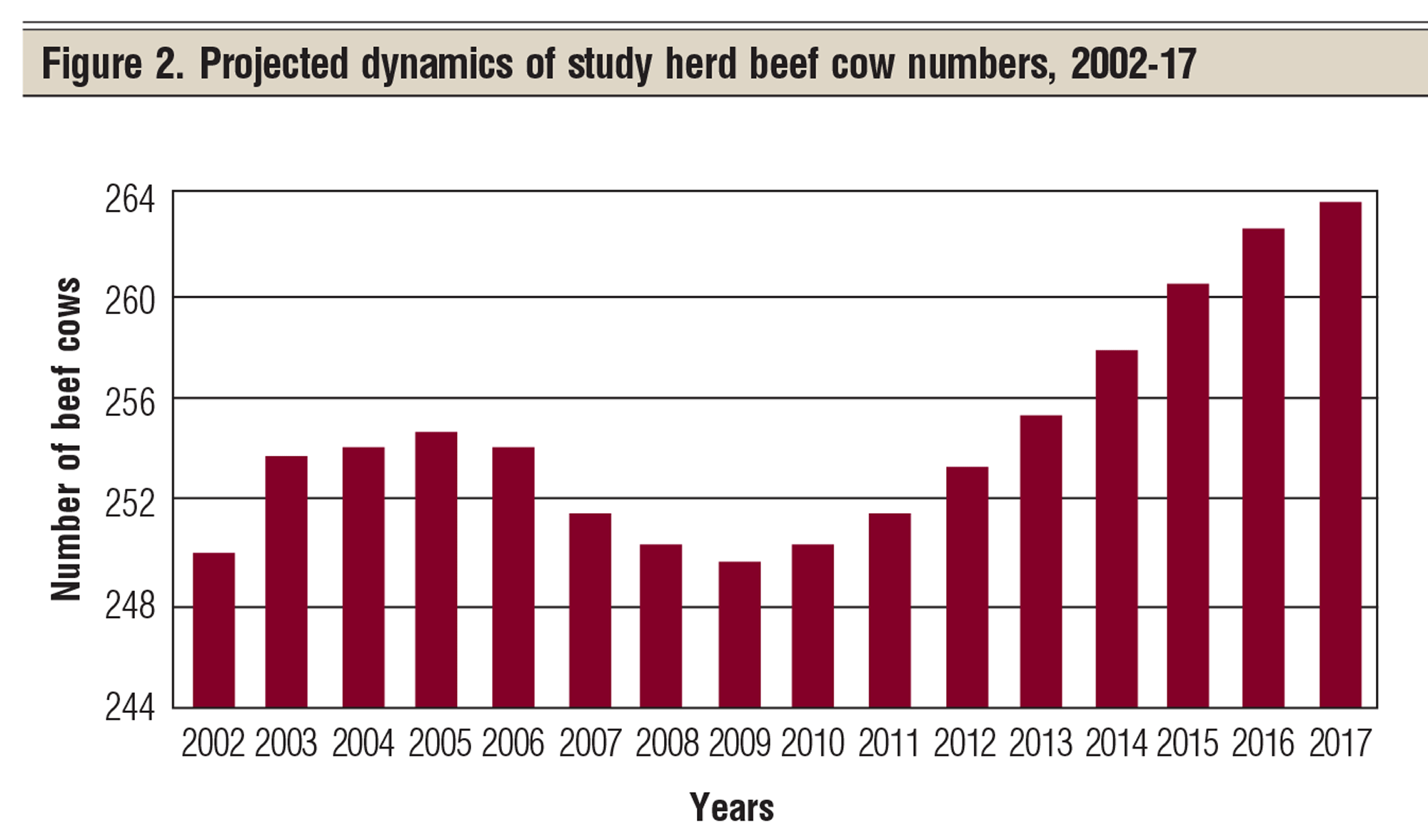

To emphasize the significance of changing culling rates and changing replacement rates, I will apply these benchmark culling rates and replacement rates to my eastern Wyoming/western Nebraska study herd (see Figure 2).

What if this herd started out in 2002 as a 250-cow herd and then followed the CHAPS database culling rates and replacement rates through time? Figure 2 presents the projected cow number pattern for my study herd from 2002 through 2017. If the rest of the nation follows this pattern, we have cattle cycles driven by culling rate and replacement rate.

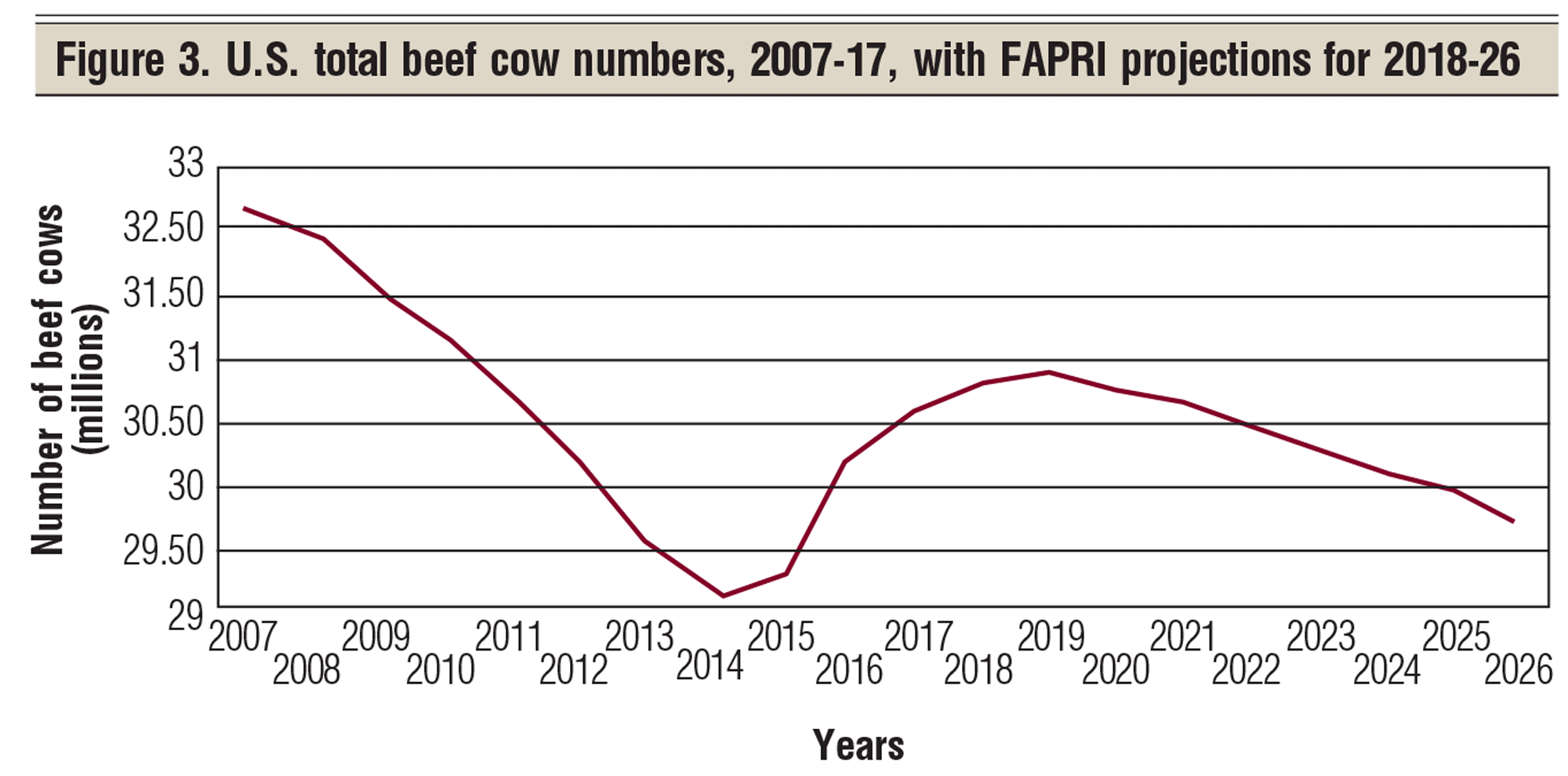

Let’s now expand our discussion to the national beef cow herd and the impact of the national culling rate and replacement rate. Figure 3 presents the U.S. total beef cow herd from 2007 through FAPRI’s projections out to 2026. FAPRI is the Food and Agricultural Policy Resource Institute at the University of Missouri.

These data suggest that since the low of 2014, beef cow numbers have been increasing. While it is hard to project future weather impact on the nation’s beef cow herd, the current projections are that beef cow numbers will again increase in 2018 and again in 2019 — albeit at a slower expansion rate.

The increase in cattle prices in November 2017 probably guarantees replacement rate will exceed the culling rate at least in 2018 and probably again in 2019. If this happens, herd expansion will surely put pressure on calf prices for the next couple of years.

I suggest that heifers born in 2018-19, which are developed, should calve during the peak of the next price cycle.

Final food for thought

Heifers born during the low part of the beef price cycle tend to produce calves during the high part of the beef price cycle. Heifers born during the high part of the beef price cycle tend to produce calves during the low part of the price cycle.

Stay tuned.

Leave A Comment