Livestock Market Information Center

The bulk of U.S. beef cattle operations wean calves in the fall months, and that is also when they select cows for culling and begin to sell them. Many cow-calf operations in the drought impacted northern High Plains states have already pregnancy checked their cows, which is earlier than normal. Most of those cows already have or will soon be sent to market.

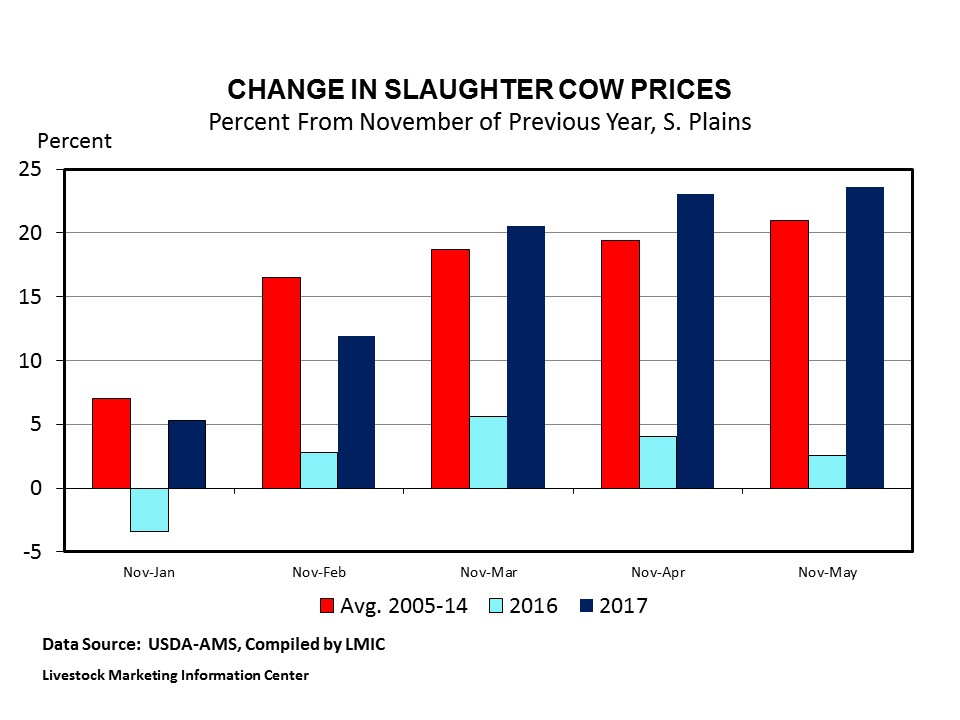

Over a cattle inventory cycle (typically 10 to 11 years), seasonally cull cow prices typically are lowest in the fourth (fall) quarter of the calendar year (usually November and sometimes October or December). The long-term average decline in cull cow price is about 10% between September and November — last year’s drop in the Southern Plains was 19% (about $13.25 per cwt.). (Note that in 2016, December posted the lowest cull cow price.) Then prices rise into the new calendar year, often rather dramatically. But in some years, the new calendar year does not bring much, if any, price increase. Holding cull cows did not pay from the fourth quarter of both 2014 and 2015 into the next year. Last year (between November 2016 and the first several months of 2017), the normal seasonal price increase returned. In 2016, per cwt. price increases were $5.25 between November and January; $12.00 November-February; and $20.50 November-March. Several factors underpin the seasonal pattern in cull cow prices. First, as already mentioned, the supply of cull beef cows is largest in the fall which dampens prices and after those large supplies are marketed prices increase. Second, fed cattle prices are typically highest in the winter and early spring months (i.e., February through May) which supports slaughter cow prices. Other factors that can significantly influence cull cow prices are the level of dairy cow slaughter and the amount of beef imported from Australia and New Zealand (that beef competes mostly in the “cow-beef” market and not as much with meats from fed steers and heifers).Cull cow prices this fall are expected to decline compared to recent levels by average percentages. Forecasts are that fed cattle prices into the first few months of 2018 will strengthen, but remain below 2017’s levels. Levels of beef imports and national dairy cow slaughter may be slightly higher year-over-year (due to lower milk prices received by producers) but are not forecast to be enough to take all the seasonal increase in cull cow price away. Cull prices into early 2018 are forecast to increase, but not reach the levels of early 2017. Cow-calf producers that are set-up to economically add some weight to cull cows and then sell in the first few months of 2018 instead of this fall at the seasonal price low, might want to put a pencil to that soon.

Several factors underpin the seasonal pattern in cull cow prices. First, as already mentioned, the supply of cull beef cows is largest in the fall which dampens prices and after those large supplies are marketed prices increase. Second, fed cattle prices are typically highest in the winter and early spring months (i.e., February through May) which supports slaughter cow prices. Other factors that can significantly influence cull cow prices are the level of dairy cow slaughter and the amount of beef imported from Australia and New Zealand (that beef competes mostly in the “cow-beef” market and not as much with meats from fed steers and heifers).Cull cow prices this fall are expected to decline compared to recent levels by average percentages. Forecasts are that fed cattle prices into the first few months of 2018 will strengthen, but remain below 2017’s levels. Levels of beef imports and national dairy cow slaughter may be slightly higher year-over-year (due to lower milk prices received by producers) but are not forecast to be enough to take all the seasonal increase in cull cow price away. Cull prices into early 2018 are forecast to increase, but not reach the levels of early 2017. Cow-calf producers that are set-up to economically add some weight to cull cows and then sell in the first few months of 2018 instead of this fall at the seasonal price low, might want to put a pencil to that soon.

Source: The Stock Exchange News